quantpedia the encyclopedia of quantitative trading strategies

How doh we create strategies

We are continually building a database of ideas for quantitative trading strategies derived out of the academic research papers.

We read a heap of papers, select the best and extract trading rules in manifestly language, performance and risk characteristics and single other synchronous attributes.

Selected strategies are then added into the alive Quantpedia body structure. Users can screen categorized strategies, examine related strategies operating theatre inspection unreal comparisons.

Quantpedia has curated an stately collection of strategies settled on academic explore, covering styles, industries and plus classes from around the world. It is a worth imagination to whatsoever financial organisation seeking to improve their reason.

Jared Liberal

QuantConnect

CEO danamp; Founder

Quantpedia provides plenty of inspiration. I'm continually impressed with how the place is well-kept to date with fresh strategies and features. The team up do not sugarcoat anything. They present complete the important facts so you force out quickly understand a scheme and get to work.

J. B. Marwood

independent monger,

investor danamp; writer

A very useful tool for quantitative portfolio managers to get raw ideas for military science asset allocation strategies.

Igor Vilcek

VUB Generali

Important Investment Officer

See examples!

Browse our free strategies

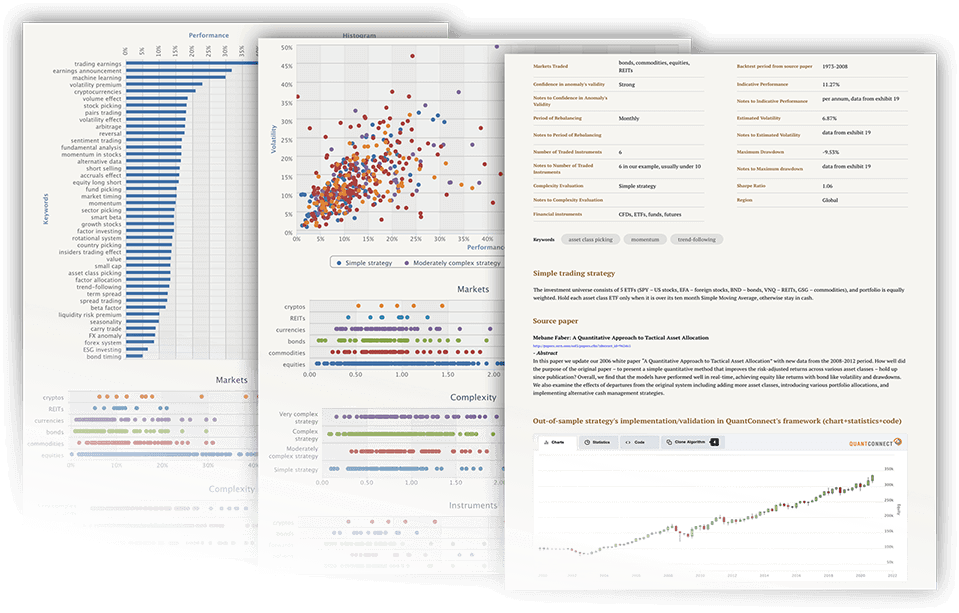

| Title of Strategy | Period of Rebalancing | Markets Traded | Indicative Performance | Volatility | Keywords |

|---|---|---|---|---|---|

| Asset Class Trend-Following | Monthly | bonds, commodities, equities, REITs | 11.27% | 6.87% | asset class pick, impulse, trend-following |

| Time Series Impulse Set up | Monthly | bonds, commodities, currencies, equities | 20.7% | 15.74% | factor out investment, momentum, smart beta |

| Payday Anomaly | Daily | equities | 2.57% | 4.31% | market timing, seasonality |

| Skewness Effect in Commodities | Unit of time | commodities | 8.01% | 10.2% | cistron investing, smart beta, volatility effect |

late feature

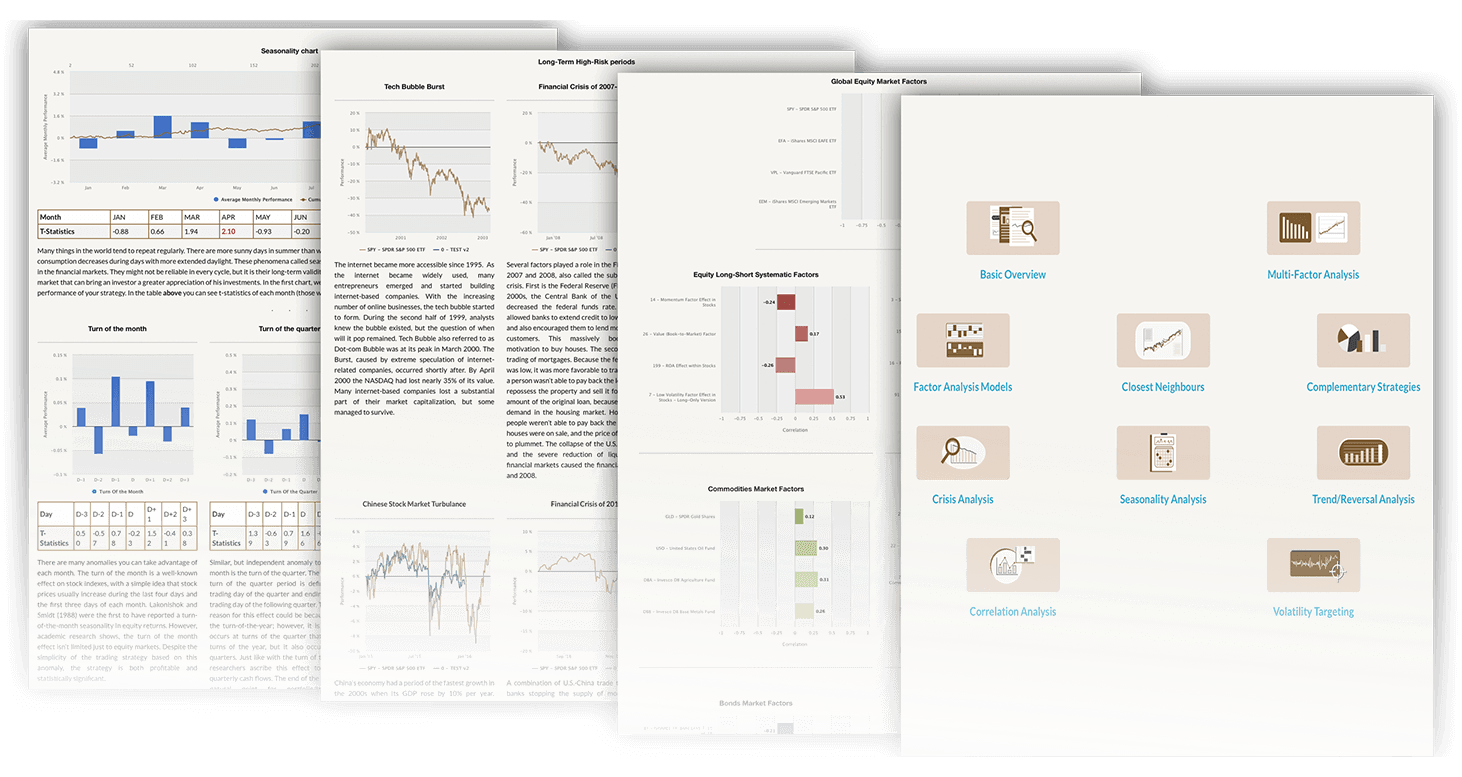

Quantpedia In favor allows users to combine Quantpedia model strategies, passive market factors and custom equity curves to build multi-factor and multi-scheme model portfolios. Users can analyze posture portfolios and their performance, relationships, assembling, factor exposures, correlations and market risks.

Subscribe for Newsletter

Be low gear to know, when we release new content

Backlog in

quantpedia the encyclopedia of quantitative trading strategies

Source: https://quantpedia.com/

Posted by: cannonquichishipt.blogspot.com

0 Response to "quantpedia the encyclopedia of quantitative trading strategies"

Post a Comment